Get. Gather. Go.

Paycheck Protection Program

SBA Loan Program for Small Businesses

The Coronavirus Aid, Relief, and Economic Security (CARES) Act allocated $349 billion in 100% federally guaranteed loans to small businesses including many non-profits. Known as the

Get. Gather. Go.

We want to be sure that all eligible businesses in the Ocala Metro are ready to apply for this new loan with their bank or credit union when applications are open on April 3.

Click Here for a Loan Guide - updated!

On April 23, the Congress approved another $310 Billion for the Paycheck Protection Program. If you were not funded in Round 1, here are some suggested steps:

- If you submitted an application to your lender, PLEASE follow up with them. Many lenders have been prepping their pipelines with applications that did not get through the first round. Your lender may be planning to submit your application in this second round so please contact them before you apply again.

- If you did not submit an application in the first round, please get your application and support documents ready NOW. The system has been built and many lenders have applications ready to go. Fewer lenders will be participating in the second round because they have reached their lending caps. The following is a list of lenders* who have indicated they are still taking new applications (some are requiring you be an existing customer):

- Florida Credit Union

- Citizens First Bank

- First Federal Bank

- Columbia Bank

- Mainstreet Community Bank

- CenterState Bank

- BBVA

- Wells Fargo

*Other lenders may be taking new applications, these are the ones who have indicated this to the CEP.

Get Informed

Paycheck Protection Program Information Sheet for Borrowers Updated! 04.03.20

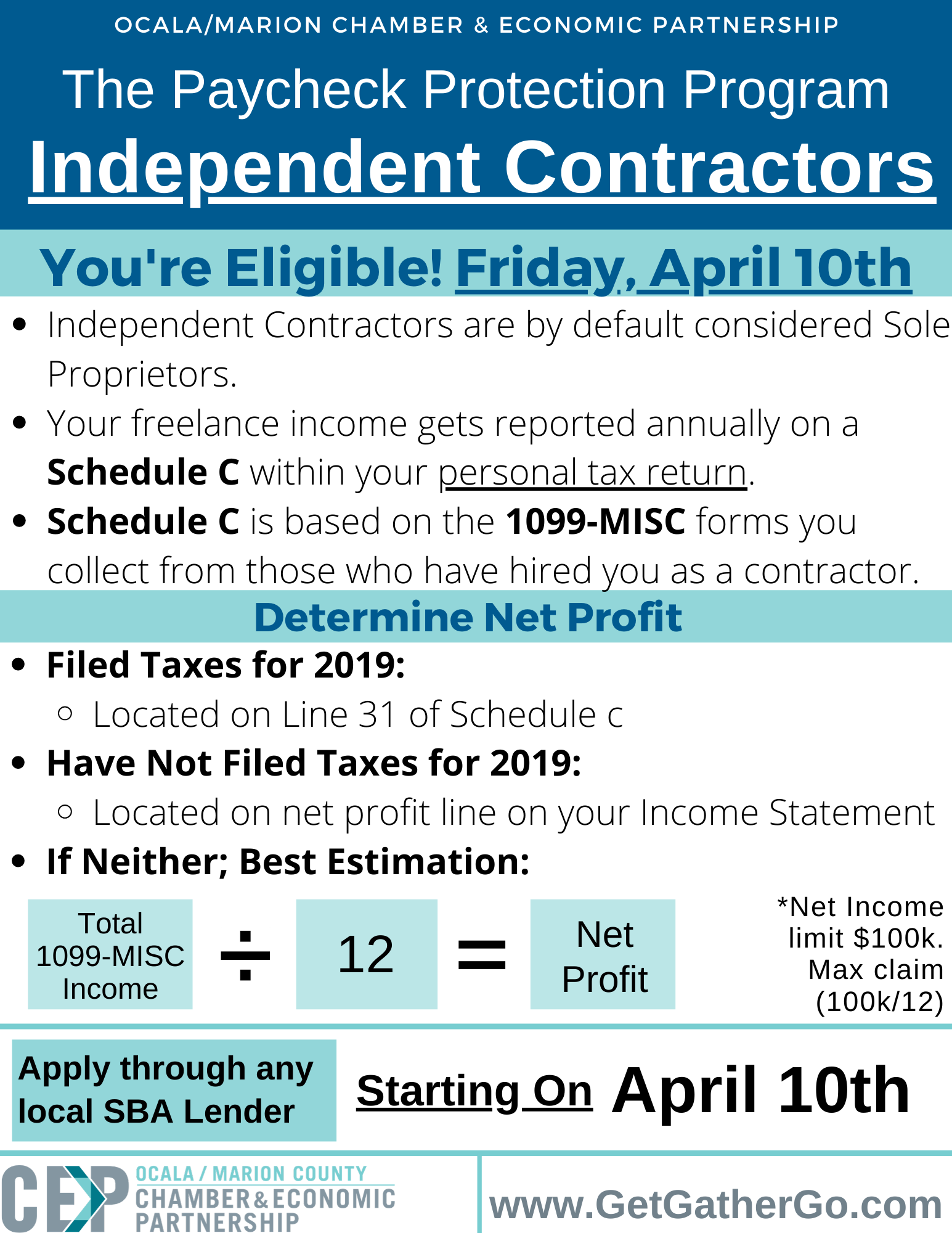

Who is eligible? A small business with few than 500 employees, including 501(c)(3)s, sole proprietors, and independent contractors.

What are lenders looking for? That the business was in operations before February 15, 2020 and had employees they paid salaries and payroll taxes for. NOTE: No personal guarantees or collateral are required for the loan.

How can the funds be used? Employee wages, commissions, and cash tips, or equivalent payments. Additionally, loans may be used for group healthcare benefits, mortgage payments, rent, and utility payments. 75% of the loan funds MUST be used on payroll and payroll-related costs.

How much can be borrowed? Loans can be up to 2.5 times the borrower's average monthly payroll costs, not to exceed $10 million.

How does the loan forgiveness work? Borrowers are eligible for forgiveness equal to the total amount borrowers spent on the following items during the 8-week period beginning on the date of the origination of the loan: payroll costs, interest on mortgage(s), rent, and utility payments.75% of the funds must be used on payroll and payroll-related costs.

How could the forgiveness be reduced? You will owe money if you do not maintain your staff and payroll. Not more than 25% of the forgiven amount may be for non-payroll costs.

- Number of Staff: Your loan forgiveness will be reduced if you decrease your full-time employee headcount.

- Level of Payroll: Your loan forgiveness will also be reduced if you decrease salaries and wages by more than 25% for any employee that made less than $100,000 annualized in 2019.

- Re-Hiring: You have until June 30, 2020 to restore your full-time employment and salary levels for any changes made between February 15, 2020 and April 26, 2020.

What is the interest rate and term if it is not forgiven? The loans carry a 2-year term at 1% interest with no payment for the first 6-months from funds disbursement though interest will accrue during this time.

Can I apply for other CARES Act benefits? No.Taking a loan under the Payroll Protection Program and/or having all or part of such a loan forgiven makes an employer ineligible for certain other relief under the CARES Act. For example, the payroll tax relief that is otherwise available under the CARES Act is not available to an employer that takes advantage of the Payroll Protection Program.

Additional Frequently Asked Questions from the Treasury.

For more information, you can review the SBA's Interim Final Rule for this program.

Gather Your Documents

Here is the list of documents that it is anticipated you will need for the applications. Start gathering them now!

-

Completed Loan Application Updated! 04.03.20

- Payroll Expense verification documents to include:

- IRS Form 940—Employers Annual Federal Unemployment Tax Return (https://www.irs.gov/forms-pubs/about-form-940) and Form 941—Employer’s Quarterly Federal Tax Return (https://www.irs.gov/forms-pubs/about-form-941)

- Payroll Summary Report with corresponding bank statement

- If a Payroll Summary Report is not available, Employee Pay Stubs as of February 15, 2020 (or corresponding period) with corresponding bank statement, and,

- Breakdown of payroll benefits (vacation, allowance for dismissal, group healthcare benefits, retirement benefits, etc.

Here are items that may be requested from your bank and will be required for the forgiveness portion of the loan:

- Employment Verification and pay rates

- 1099s (if you are an Independent Contractor)

- Certification that all employees live within the United States. (Using I-9 Forms or E-Verify) If any do not, provide a detailed list with corresponding salaries of all employees outside the United States

- Trailing twelve-month profit and loss statement (as of the date of application) for all applicants

- Most recent Mortgage Statement or Rent Statement (Lease)

- Most recent Utility Bills (Electric, Gas, Telephone, Internet, Water/Sewer, etc.)

Watch this video from our CEO on some helpful tips as you Gather your information.

Go and Apply

Let your local bank or credit union know that you want to apply. Lenders can start taking applications for small businesses and sole proprietorships on Friday, April 3, and for independent contractors and self-employed on Friday, April 10. For a list of lenders who have notified the CEP that they are participating, please click here.

CEP - Payroll Protection Program Webinar from Ocala/Marion County CEP on Vimeo. There have been slight updates to the Program since this webinar so please review the other information on this site as well.

Gather Your Documents

-

1099-Misc forms

-

Tax Return

-

Copy of your driver's license and SSN

CARES Act Relief for Independent Contractors

If you are an independent contractor or self-employed individual, you may be eligible for Paycheck Protection Program (PPP) loans/grants, SBA’s Economic Injury Disaster Loans (EIDL), and/or Unemployment Compensation for losses of income related to the coronavirus pandemic.View this Guide in English. Leer en Espanol.